Nowadays, many restaurants can’t afford to abstain from delivery. Even before 2020, online food delivery was a $94 billion market with an annual growth rate of nearly 10% and an estimated market of $134 billion by 2023, according to QSR Magazine. The global food delivery mobile app market is expected to hit $16.6 billion by 2023, with a staggering compound-annual growth rate of 27.9 percent.

However, according to the National Safety Council, in 2018 alone, there were 4.5 million medically consulted driver injuries in the U.S. that cost $445.6 billion.

Whether you’re implementing in-house delivery, utilizing third-party apps, or both, delivery comes with its fair share of risks, such as issues stemming from auto accidents, uninsured drivers, erroneous food delivery and more. To help mitigate financial and reputational risks when it comes to delivery programs, we’ve put together our top tips for Colorado restaurants:

In-House Delivery – MVRs are your MVPs

For a business with delivery, the risk associated with a single auto accident could be enormous. One way to manage this risk is by using motor vehicle records (MVRs) to select and retain quality delivery drivers. With an MVR, the business manager can identify high-risk drivers before they are involved in an auto accident. It can also help a company improve on safety by targeting past driver behavior with future training programs. For example, if your drivers have a history of small related accidents, then a training program can be developed to reduce these incidents.

At a minimum, any company that has delivery drivers should run an MVR at the time of hire and annually thereafter to ensure they have good driving records and are properly licensed. Since MVRs are considered a type of background check, it is important to develop a company policy that has been reviewed by your legal representative. This policy should include anyone using a company-owned vehicle or a personal vehicle on company time.

A company can spend thousands of dollars in court costs and attorney’s fees if the driver-screening process is not completed appropriately. While an insurance agent may help you with some of these steps, the management and retention of quality of drivers is the basic responsibility of your business.

In addition to prioritizing MVRs, her are other tips for in-house delivery programs:

- Don’t overwhelm the delivery staff with too many orders, as this may result in unsafe driving practices.

- Deliveries to hotels should only be made to the front desk for the driver’s safety.

- Late night deliveries to locations that don’t have a valid address, such as a park or parking lot, are not safe and should be avoided.

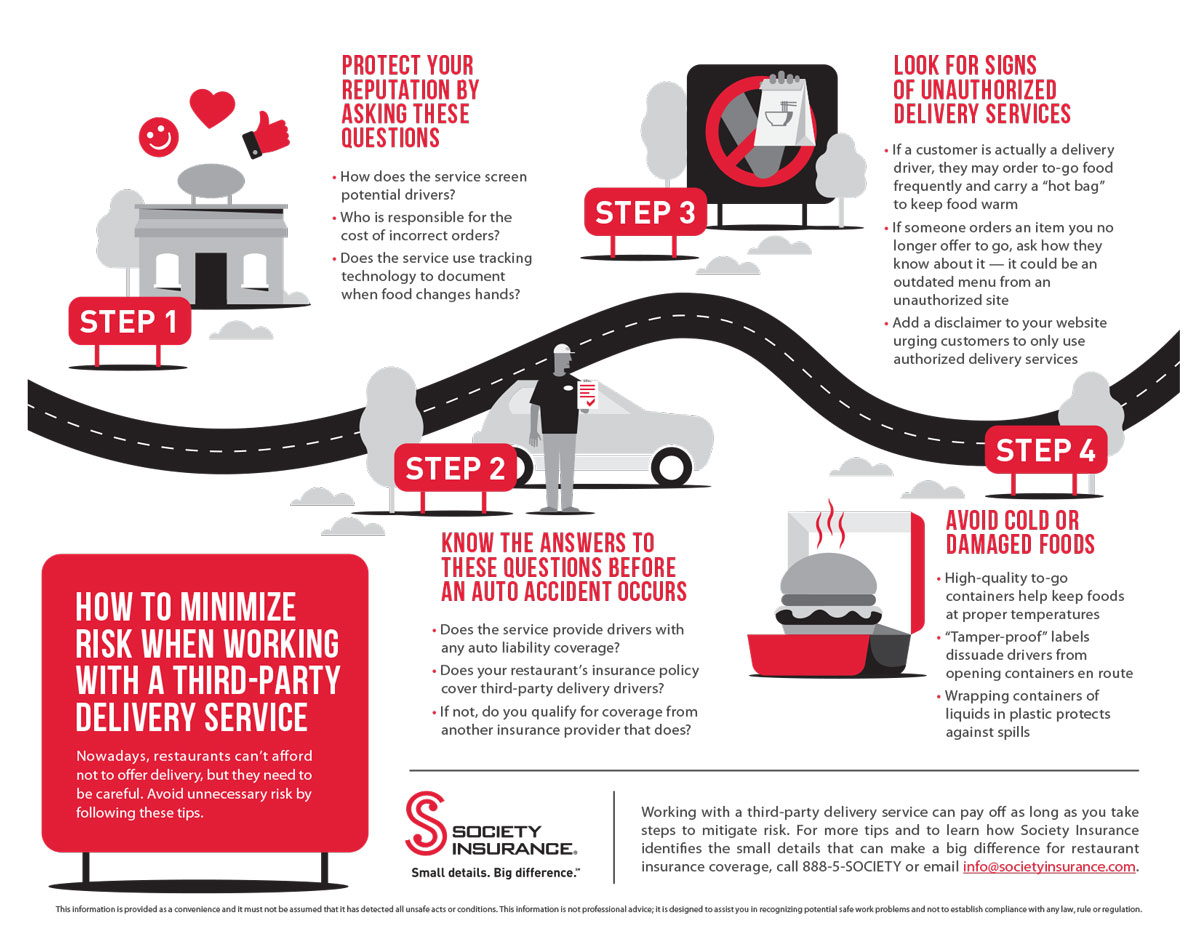

Third-Party Delivery Services – Ask the Right Questions Before Signing On

According to a recent study in Restaurant Dive, 90% of limited service restaurants are now using third-party delivery services. Another survey showed that nearly a third of Americans use third-party delivery services at least twice a week. However, it’s important to make sure that you’re aware of the potential risks when it comes to third-party delivery services so you can appropriately protect your business. Before signing a contract with one of these services, ask the following questions.

#1 Who’s liable if the driver is in a car accident?

When a driver is in an accident while delivering food from your restaurant, who is liable? Depending on the third-party delivery service, the responsible party can vary. Many services do not provide liability for drivers, as their contracts specifically state they are only providing the software that connects the restaurant to the delivery driver. In that case, there may not be any insurance outside the driver’s personal auto insurance. The driver may have a low personal limit or might have their coverage denied because food delivery is considered a commercial exposure. In these situations, the victim may turn to the restaurant to cover the costs of the accident. If you’re contracting with a third-party delivery service, let your insurance agent know. Your agent can review the contract to determine what types of insurance you may need to protect your restaurant. Additionally, your restaurant’s auto policy should be reviewed to see whether third-party delivery service is a covered exposure. If it’s not covered, your agent can help you find a policy that will provide the necessary coverage.

#2 What kind of screening do you perform for potential drivers?

When you’re working with a third-party delivery service, you can’t control who the service hires as drivers. Because of this, it’s important to learn about the company’s hiring standards to ensure it’s not hiring drivers you wouldn’t be comfortable working with. Ask how the service screens its potential drivers. Does it check motor vehicle records, perform a background check or ask about previous driving experience? If the service’s practices are too relaxed, you may want to consider a different option to minimize the chance of an incident with a delivery driver.

#3 Who is responsible for order errors?

Generally, customers using third-party delivery services are ordering their food through an online platform. When an error with the order occurs, how is that handled? Does the service allow customers to submit complaints, or are customers encouraged to reach out directly to the restaurant? Find out what kind of resources are available should your restaurant receive complaints about the delivery service so you’re able to quickly address these complaints and provide as best a customer service experience as possible.

#4 What kind of order tracking does the service offer?

Related to order errors, using a tracking technology can help determine where a poor customer experience may have gone wrong. A tracking technology that documents when the food order switched hands from the restaurant to the delivery person to the customer is especially helpful in situations dealing with foodborne illness or complaints over food quality. For example, you may discover that while your restaurant provided quick service, the delivery person took an unreasonably long time to deliver a customer’s order, and that’s why it arrived cold.

You Can Count on Society to Help Keep Your Business Safe

Whether you choose to engage a third-party delivery service, handle a delivery program yourself, or hold off on starting a delivery program, nationwide increases in delivery orders are here to stay. Society Insurance has a team of risk control experts to help strengthen your loss prevention efforts and provide sustainable real-world solutions to help make your business safe and profitable.

Society Insurance is ready to help you navigate the unique challenges facing your restaurant. Ask your local Society Insurance agent about specific coverage questions, and explore our blog for more tips and trends to help you make smart safety decisions for your business.

This information is provided as a convenience, and it must not be assumed that it has detected all unsafe acts or conditions. This information is not professional advice; it is designed to assist you in recognizing potential safe work problems and not to establish compliance with any law, rule or regulation.

Author : Society Insurance

Society Insurance offers top-notch insurance coverage and service to select businesses in Colorado, Georgia, Illinois, Indiana, Iowa, Minnesota, Tennessee, Texas and Wisconsin. As a mutual insurance company, we have been policyholder-owned for over 100 years. We take pride in getting your coverage right—right from the start— with a unique combination of property and casualty coverages in one comprehensive package.